Taxes & Legal

Successfully establishing your own foundation: Guide and success factors

This blog article deals with the topic of foundations and what motivations, steps, and challenges there can be for a successful establishment.

—

12 minutes

In this text, we would like to bring you closer to the definition and key aspects of foundations and the founding process. You will also find information here on how cost and resources can be effectively deployed to focus on the essentials.

📚 Contents

What is a foundation?

For whom can establishing a foundation be useful?

Motives for establishing a foundation

Disadvantages of a foundation

Founding your own foundation: Understanding the basics

Possible legal forms for foundations and suitability

Saving taxes? What benefits foundations really bring with them.

Overview of the different types of foundations

Legal requirements in detail

The path to your own foundation: Step-by-step

Costs of a foundation: Incorporation and ongoing expenses

Successful foundation administration

The easiest way - The Online Foundation

Summary of the most important points

References to further literature and resources

What is a foundation?

The definition is largely identical to the one found in the encyclopedia 150 years earlier. Accordingly, a foundation is an asset of value (in the first instance capital, but real estate and other objects of value can also be meant here) of which the founder divests themselves permanently and irrevocably and binds it to a purpose, with its own legal form. This is also how it is stated in the Civil Code (§ 80 paragraph 1):

The foundation is a memberless legal entity equipped with assets for the permanent and sustainable fulfillment of a purpose specified by the founder. The foundation is usually established for an indefinite period, but it can also be established for a specific period during which all of its assets must be consumed to fulfill its purpose (consumable foundation).

A "legal entity" is a legal term that refers to an organization or company that is recognized by law as an independent entity and can therefore have rights and obligations, similar to a natural person (meaning a human being). Legal entities can enter into contracts, sue and be sued, own property, and be subject to taxation.

💡Did you know? The term 'foundation' is not legally protected

It must be said at the outset that the term foundation is not protected. Accordingly, one can call a GmbH a foundation, one can call a trust foundation a foundation, and political foundations are also mostly organized as associations, but call themselves foundations in public. A foundation fund can also easily be called a foundation.

For whom can establishing a foundation be useful?

In principle, anyone is free to establish a foundation, whether it is a natural person or a legal entity such as a business or a legal association.

If a specific non-profit purpose is to be pursued in the long term or assets are to be assigned to a specific purpose over generations, establishing a foundation is recommended. This is particularly suitable for:

Businesses: Establishing a foundation can serve to guarantee the continuity of a company or protect the assets of a - for example - family business from potential conflicts regarding inheritance. However, a non-profit foundation can also be used as part of the Corporate Social Responsibility (CSR) strategy.

Heirs: People who possess large assets and want to ensure that their heritage does good over generations or is used for another specific purpose can provide for a foundation in their will. This makes it possible to use assets for non-profit purposes to convey philanthropic ideas and values to the next generations and to work together on them.

Family foundations: Families can jointly establish a foundation to support their common values and goals for non-profit purposes.

Public figures

Foundations certainly also fulfill a legitimization function here in order to publicly project the commitment of a private person, a family, or a company (if desired) in a transparent and trustworthy manner. This is also favored by the prevailing control mechanisms that apply to hold the status of a non-profit foundation - and thus also various tax benefits.

In summary: A foundation is suitable if a specific non-profit purpose is to be pursued in the long term or if assets are to be dedicated to a specific purpose over generations. Foundations can also make sense for tax optimization as part of estate planning. The areas of application of a foundation are extremely versatile, and the idea can be applied to a variety of other projects by different initiators. It is indeed extremely confusing what a foundation actually is. We are trying to bring light into the darkness.

💡Did you know? Foundations in comparison

In contrast to associations, which have their member base, and GmbHs, which have their shareholders as sponsors, a foundation is based on assets that are permanently used for the foundation's purpose. A very important aspect of a foundation is its independence, as a foundation is not dependent on its members or shareholders.

Foundations also often enjoy high prestige, which can facilitate access to donors, partners, and public support, and they enjoy tax benefits, especially if they pursue charitable purposes.

Motives for establishing a foundation

There are foundations and foundation-like structures that have survived for hundreds of years and still exist today. Even if the term foundation cannot always be clearly defined, there are nevertheless central motives that drive people to establish one today.

Promoting the common good: Through independent and long-term funding, foundations can support charitable projects across all impact goals throughout political cycles and bring about sustainable changes. In addition, they strengthen civil society by also involving local initiatives and enabling voluntary engagement. In times of crisis, they also offer quick, unbureaucratic help where state support may not be sufficient.

Tax benefits: As described above, charitable foundations can reduce the tax load for various reasons.

Protection of assets: Foundations are excellent for protecting assets because they secure assets in the long term and protect them from fragmentation or uncontrolled distribution, such as with family foundations, which minimize inheritance tax burdens, or corporate foundations, which secure corporate assets in the long term.

Disadvantages of a foundation

After the foundation is established and recognized, dissolution is only possible under very strict conditions. For example, if the foundation's purpose can no longer be fulfilled or the assets are depleted. An online foundation can be dissolved at any time.

The articles of association of the foundation bind it to the defined purpose; changes are difficult to make. Even if societal needs or the founder's priorities change over time, the foundation remains obligated to manage and deploy the assets in accordance with the originally defined purpose. Thus, a foundation established many years ago with the goal of education cannot easily reallocate its funds to address environmental issues, for example.

One should also know that establishing a foundation is usually associated with high costs and stricter legal requirements must also be met. This means high bureaucracy, accompanied by advisory effort - for example through reporting to the tax office or the foundation authority. Coordinating service providers - such as wealth advisors, notaries, or tax advisors - requires significant financial resources as well as a lot of time, which can deter many potential founders.

ℹ️ The situation is different for digital foundations, which offer significantly greater flexibility and lower associated costs.

Founding your own foundation: Understanding the basics

The number of legally independent foundations has risen continuously since 2011, and in 2022, 25,254 foundations in Germany were counted. 95 percent of all foundations have charitable, benevolent, or church purposes and benefit from corresponding tax exemptions, which ensure that the foundation assets can be fully used for the foundation's purpose.

If you are considering founding your own legally independent foundation, you should first familiarize yourself with the basic terms and requirements.

Legal requirements for foundations at a glance:

The foundation requires articles of association regulating the foundation's purpose, the governing bodies, and asset management. The contributed assets must be sufficient for the foundation's purpose to be pursued permanently. A foundation only gains its legal capacity through recognition by the competent foundation authority. These prerequisites do not apply when establishing an online foundation.

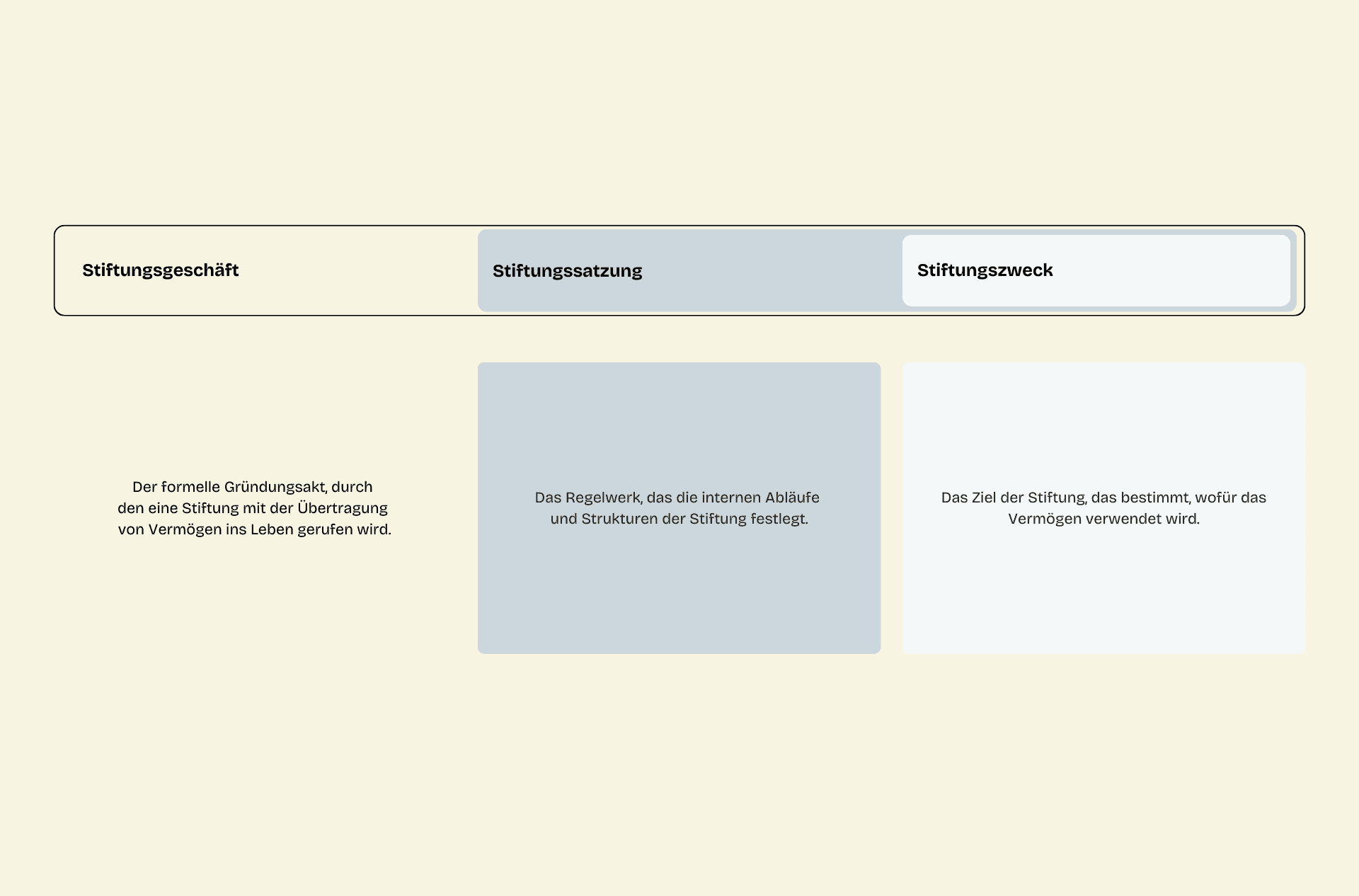

Founding deed

The founding deed (Stiftungsgeschäft) is a fundamental component and condition for establishing a legally capable foundation under civil law. It can be equated with the declaration of intent of the founder, in which the wish is expressed to a) set up a foundation and b) provide specific assets or any property values for this purpose. In this process, the foundation authority is requested to review and, if applicable, grant this approval. Therefore, the founding deed is often also viewed as an application for foundation approval.

Summary: The founding deed is the comprehensive act of creation, and the articles of association (including the foundation purpose) are an important part of it.

Articles of association and foundation purpose

The articles of association (Satzung) are the central document of a foundation. The foundation's purpose is documented and bindingly defined here. Furthermore, it contains:

- Name of the foundation and registered office

- Assets and/or other tangible property values

- Foundation organs, such as the executive board and, if applicable, supervisory bodies like foundation councils

The foundation purpose is the heart of every foundation and determines which goals and purposes are to be pursued in the long term. It is recorded in the articles of association of a foundation and is not only important for the orientation of the foundation's content, but also for its legal recognition, especially if tax exemptions are sought. For this, the purpose must serve charitable, benevolent, or church goals. These goals must accordingly be clearly defined in the articles of association and aligned with the requirements of the German Fiscal Code (§§ 51 ff. AO).

Examples of (charitable) foundation purposes:

🏫 Promoting education: Supporting educational institutions, scholarship programs for students, supporting educational initiatives in disadvantaged regions.

🌻 Environmental protection: Preserving biodiversity, promoting sustainable agriculture, supporting projects to reduce CO2 emissions.

🏰 Cultural promotion: Preservation of cultural assets, supporting artists, promoting cultural education.

👨👩👦 Family foundations: are a special form of foundation that is often not tax-exempt and usually serves to preserve a specific asset over the long term.

Important notes and tips

Foundation purpose and articles of association

Clarity and precision: The purpose should be formulated clearly and precisely to avoid misunderstandings. The more specific the purpose, the better it can be implemented in practice and legally secured.

Immutability: All decisions of the foundation's organs must inevitably align with the foundation's purpose. This remains (mostly) permanently active and cannot be changed over time, unless it can fundamentally no longer be achieved.

Investment strategy: The foundation's capital is invested in a targeted manner to support the charitable purpose through the generated income. In the articles of association, you can determine if you want to exclude, for example, certain financial products or industries.

Therefore, flexibility for future adjustments: Consider including a clause in the articles of association that makes it possible to adjust the purpose of the foundation or to keep some doors open through the phrasing.

Coordination with the foundation supervision: The draft of the articles of association is usually coordinated with the competent foundation authority and the tax office (regarding tax exemption) to ensure that all legal and official requirements are met.

Foundation assets

The foundation assets include the capital made available to a foundation upon its establishment or through subsequent donations and used to fulfill its charitable purpose. It usually consists of financial funds, securities, real estate, and other assets.

This capital is invested in the long term a) to generate income that finances the foundation's activities and is thus b) preserved to ensure the fulfillment of the foundation’s purpose. Learn more about this later.

Possible legal forms for foundations and suitability

The term foundation is not bound to a specific legal form, and the decision on the best choice depends, as so often, on various factors. For example, it can be used to determine the tax deductibility of donations, legal independence, or the decision-making relationships of different stakeholders within the foundation.

The legally capable foundation under civil law and the trust foundation are very popular for foundation projects - but foundation-like entities such as a GmbH or an association also occur.

Legally independent foundation under civil law: Independent legal entity.

Trust foundation: Managed by a trustee, but is not legally independent.

Foundation gGmbH: Combination of foundation and limited liability company.

Choosing the legal form for a foundation is a crucial step that depends on the generator's goals and needs. It is important to note that each legal form carries different legal, financial, and organizational implications.

Legally independent foundation under civil law (Stiftungen des bürgerlichen Rechts)

Characteristics:

Own legal personality: This foundation is an independent legal entity and can independently enter into contracts, sue, and be sued.

Independence: It operates independently of the founder once established and is managed by an executive board.

State supervision: It is subject to foundation supervision by the competent authority of the federal state in which it was established.

Easy to combine with tax exemption

What is this legal form suitable for?

Long-term and permanent purposes: This legal form is particularly suitable for founders who want to pursue a permanent purpose that exists independently of themselves.

High administrative burden: The legally independent foundation requires a certain administrative overhead and is suitable for larger assets to be managed in the long term.

Charitable purposes: Frequently chosen when the foundation's purpose is charitable and tax benefits are sought.

Trust foundation (Non-legally independent foundation)

Characteristics:

No own legal personality: The trust foundation is not legally independent. It is managed by a trustee who holds the foundation's assets on a fiduciary basis.

Flexibility: This form offers flexibility as it is less formalized and can be set up more quickly.

Founder connection: The founder can maintain a stronger connection to the foundation, as the trustee works closely with them.

What is this legal form suitable for?

Smaller assets: Suitable for founders who can or want to contribute only smaller assets.

Less administrative burden: Ideal for founders who prefer structured and simpler administration and have no need for a complex organizational setup.

Short-term or specialized projects: Often chosen when the foundation's purpose is of a shorter-term nature or supports highly specific projects.

💡Did you know that the question of the legal form does not always have to be asked?

For example, you do not have to establish your own trust foundation, but can simply use the infrastructure of existing trust foundations, into which you can easily establish a foundation fund. Even with charitable, private foundations, many advantages can already be used by establishing an online foundation.

Foundation GmbH or gGmbH

Characteristics:

Legal personality: The foundation GmbH is a GmbH that can be linked with a non-profit purpose (then gGmbH).

Management: Management is conducted by the managing directors of the GmbH, and it is subject to the usual regulations of the GmbH Act.

Flexibility: Here, the flexibility of a GmbH can be combined with the tax benefit of a non-profit organization.

What is this legal form suitable for?

Combination of entrepreneurial and charitable goals: Ideal for founders who, in addition to a charitable purpose, also want to pursue entrepreneurial activities.

Simple structure: For founders who prefer a simplified legal form that nevertheless offers its own legal personality.

Tax advantages: If tax benefits from charity status are desired, but an entrepreneurial structure is to be maintained at the same time.

Foundation Association (Stiftungsverein)

Characteristics:

Legal personality: A foundation association is a registered association (e.V.) that pursues a specific foundation purpose.

Member structure: The organization is supported by members who also influence decision-making processes.

Flexibility: It offers high flexibility and can be easily adapted to changing circumstances.

What is this legal form suitable for?

Member-based activities: Suitable for projects where the participation of many members and a democratic decision-making process are important.

Charitable and social purposes: Often chosen for social projects or local initiatives where the foundation purpose is pursued through the active engagement of members.

Exemplary foundations, their legal form, and impact

Schwarzkopf Foundation Young Europe

Legal form: legally independent foundation under civil law (charitable)

Impact: The foundation was established to promote European integration and give young people in Europe a voice. It organizes exchange programs, discussions, and educational projects dealing with European topics. The foundation enhances understanding and cooperation between young Europeans and strengthens European identity.

Robert Bosch Stiftung

Legal form: GmbH

Impact: It supports research projects, educational initiatives, health programs, and cultural events. It also promotes social cohesion and international cooperation to bring about positive societal changes.

Neven Subotic Foundation

Legal form: legally independent foundation under civil law (charitable)

Impact: Established by football player Neven Subotic, this foundation works for access to clean drinking water and education in Africa. Focusing on rural areas in Ethiopia and Kenya, the foundation builds wells and sanitary facilities to sustainably improve the living conditions of the local population.

Saving taxes? What benefits foundations really bring with them.

The reputation of serving as a tax-saving vehicle precedes foundations. But what is really true about the myth? Fundamentally, the most important distinction here is: Charitable or private benefit?

Tax advantages for charitable foundations

If a foundation is recognized as charitable, it enjoys extensive tax benefits. These include:

Exemption from corporate income tax: A charitable foundation does not have to pay corporate income tax on its earnings.

Exemption from trade tax: Since a charitable foundation does not pursue commercial purposes, trade tax is also omitted.

VAT exemption: Certain activities of a charitable foundation can be exempt from value-added tax.

Asset transfers to a charitable foundation are exempt from inheritance tax and gift tax. This means that a founder can bring assets into the foundation tax-free, which represents a significant tax saving, especially with larger assets.

If the foundation generates investment income (e.g., from renting, leasing, or capital yields), this income is generally exempt from taxation for charitable foundations, provided it is used within the scope of charitable activity.

Tax deductibility of donations to charitable foundations

Individual donations: Donations to a charitable foundation can be deducted from the donor's income tax. Private individuals can claim up to 20% of their total income as a donation.

Large donations: In addition to normal donations, founders can deduct an amount of up to 1 million euros (or 2 million euros for married couples) as a special expense over a period of ten years from their taxes. This regulation is particularly beneficial if someone contributes larger amounts to a foundation. This regulation only applies to donations to a legally independent foundation under civil law.

Tax advantages for private-benefit foundations

For private-benefit foundations, such as family or corporate foundations, the tax advantages are limited compared to charitable foundations.

They are generally subject to corporate income tax and trade tax, and asset transfers can be subject to inheritance or gift tax. Nevertheless, they offer options for tax structuring, for example for long-term asset protection within a family. These foundations can help optimize tax loads over generations by binding assets and distributing returns to the family instead of inheriting them "directly."

In reality, however, a foundation is first and foremost an instrument for long-term asset protection and usage, not primarily a tax-saving model.

On the subject of foundations, taxes, and what advantages you can actually expect when establishing one, we recommend our blog article:

👉 Tax advantages of foundations - What is true about the tax-saving myth?

Overview of the different types of foundations

Charitable foundations

These foundations are the most common form. The purposes a foundation can pursue include all purposes listed in the German Fiscal Code (AO). These include, for example, education, science, or environmental protection. An example is the "Stiftung Lesen", which passionately campaigns for the promotion of reading.

Family foundations

Family foundations primarily serve to secure and manage the assets of a family. They offer the advantage of preserving and managing assets over generations.

Corporate foundations

Corporate foundations are established by companies and often serve to promote social projects that align with corporate goals.

Comparison and special features of different foundation forms

The choice of foundation form depends entirely on the founder's individual goals and needs. If you want to enjoy tax benefits, a charitable foundation is a great option for you. If, on the other hand, you want to secure your assets in the long term, a family foundation could be perfect for you. Corporate foundations can support a company's CSR strategy.

Legal requirements in detail

Requirements for the articles of association

The articles of association (Satzung) are the central document of a foundation. It regulates the foundation's purpose, organization, and management of the foundation's assets. There are some important points that should be recorded in the articles of association so that everything is arranged according to your wishes. These include, for example, the lock-in of purpose, the organs of the foundation, and the regulations on the use of assets.

Minimum assets and capitalization

For the establishment of a foundation, minimum assets are required so that the foundation's purpose can be pursued sustainably. There is no legally specified minimum level in Germany, but starting capital of at least 50,000 to 100,000 euros is recommended.

The path to your own foundation: Step-by-step

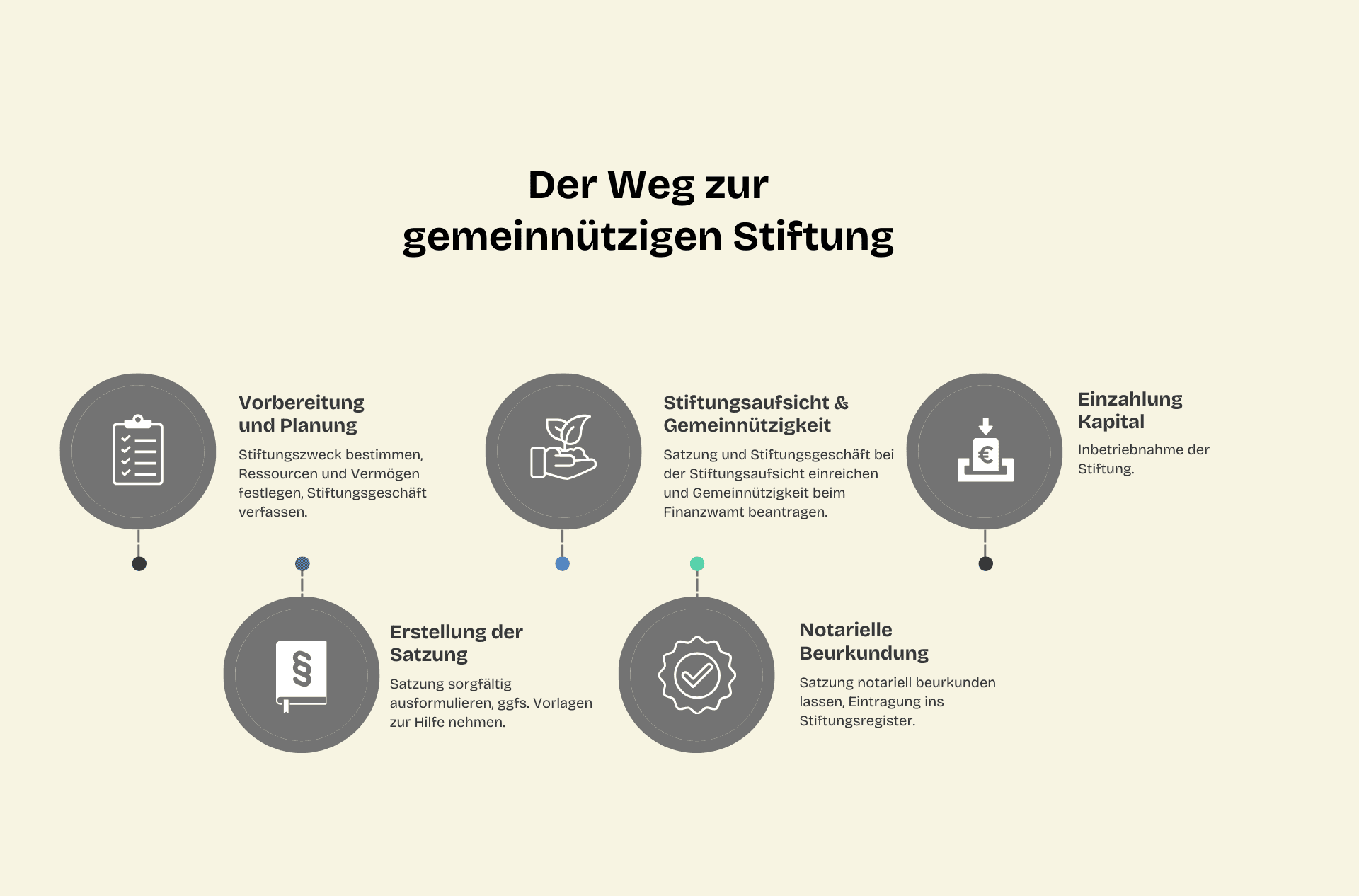

1. Preparation and planning

A foundation can be established by one or more persons. At the beginning - usually with the help of legal advice - is the precise definition of the founding deed, and thus, alongside the determination of a foundation purpose, the consideration of what resources and what assets are available to the founder. If there are several founders, they also jointly determine the purpose and the articles of association of the foundation. It is also important to consider future developments and the sustainability of the foundation.

2. Drafting the articles of association

The articles of association are the legal foundation of the foundation and should be drafted with great care so that they really cover all eventualities. Sample articles can be a great help to adopt common wordings. But don't worry if you are not entirely sure how to formulate something. The articles of association can still be individually customized; however, this is associated with additional costs.

💡Did you know? - Can a foundation be established after the founder's death?

Yes, a foundation can be established by will. The founder can specify that a foundation is established after their death, funded from their estate. Online foundations can also be created for the deceased founder without a will.

3. Notarization and registration

Once the articles of association are ready, they must be notarized and entered in the register of foundations. The costs for this vary depending on the scope of the foundation, but are often in the mid four-figure range. The authority reviews with great care whether all legal requirements are met and whether the foundation's purpose can be pursued sustainably.

Costs of a foundation: Incorporation and ongoing expenses

Incorporation costs

The incorporation costs of a foundation consist of various items. These include notary costs, fees for legal and tax consultations, and fees for registration. These costs naturally depend on the scope and complexity of the foundation.

How much capital is needed to establish a foundation? There is no legally defined minimum capital amount, but most federal states require that the foundation's assets must be sufficient to fulfill the foundation's purpose in the long term. Typically, the initial capital for a legally independent foundation is at least 50,000 to 100,000 euros, but it can be higher depending on the foundation purpose. No minimum sum is required to establish an online foundation.

An exemplary calculation could be:

Attorney costs for, for example, legal advice on drafting the articles of association and the founding deed: 2,000 - 4,000 EUR

Tax advisory costs for the recognition of charity status and tax registration: 1,000 - 2,000 EUR

Notarial costs for the notarization of the articles of association and the founding deed: 1,000 - 2,500 EUR

Foundation supervision fees for approval by the foundation supervision: 500 - 1,500 EUR

Initial capital for the foundation (e.g., 50,000 EUR for smaller foundations): 50,000 EUR (minimum capital)

Ongoing administrative costs

Ongoing administrative costs include, for example, personnel costs, office space, and general administrative expenses. These can naturally vary widely depending on the size and activity of the foundation - not every foundation, for example, has supervisory organs that may receive payment or rents an office space.

Possibilities of financing (e.g., donations, endowment contributions)

Foundations are pleased if they are funded by donations and endowment contributions (Zustiftungen). Successful fundraising can make a decisive contribution to the long-term security of foundation assets.

Successful foundation administration

Role and tasks of the executive board

The board carries the responsibility for strategic direction and operative management. A clear distribution of tasks and efficient administration are key to the success of your foundation. It is always a good idea to look at how other foundations do it.

Management of foundation assets

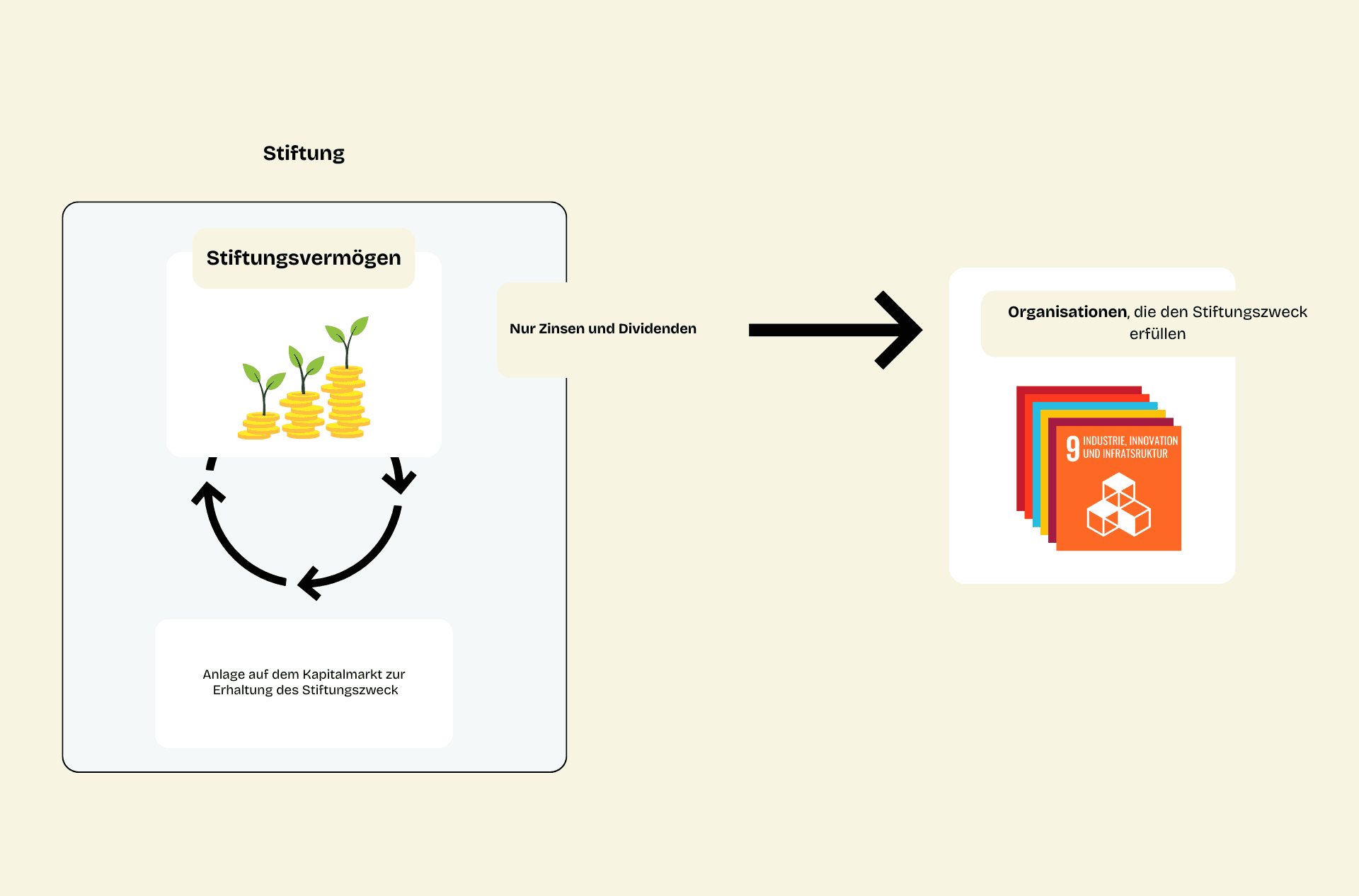

Managing the foundation's assets requires a well-thought-out investment strategy to secure the foundation's purpose in the long term.

For charitable foundations, the main assets generally remain untouched, while only the income from the invested assets is used for the good cause. This means that only interest and dividends may be used. This is to ensure that the foundation a) can exist in the long term, b) always has a stable financial basis, and c) remains capable of acting even in economically difficult times.

Responsible for asset investment is usually the foundation board, which is often supported by an investment committee. This committee often consists of experts who are familiar with financial markets and sustainable investment strategies. They must ensure that the investment strategies correspond to both the legal framework and the ethical guidelines of the foundation. The conditions from the articles of association must also be met. There, reconfiguration bans may have been imposed or asset classes excluded. Investment decisions should also be based on balanced risk management to protect foundation capital from losses while generating stable returns.

By the way, charitable foundations can also distribute up to one third of their income to the founder and their next relatives without losing their status with the tax office.

The easiest way - The Online Foundation

Even though we want to contribute with this article to bringing light into the darkness of the complex world of foundations, it becomes clear: establishing a legally independent foundation is no easy task. In addition to a certain prior knowledge, incorporation usually requires the support of external advisors and also brings little flexibility and high ongoing costs. So is our recommendation rather not to establish a foundation? Absolutely not. Rather, we would like to draw attention to a simple alternative to complex foundation establishment: establishing an online foundation on bcause.

✨ Discover the new way of doing good. Get exclusive access to the digital and free foundation guide – for engagement without bureaucracy, but with full impact.

👉 Receive the digital foundation guide now

Online foundations at a glance

Legal personality: Generally, online foundations are so-called foundation funds in an existing foundation, e.g., in a trust foundation or a foundation under civil law. A foundation fund has no legal personality of its own.

High flexibility: In comparison, an online foundation offers maximum flexibility, as there is no need to commit to a single foundation purpose, but various purposes can be supported at once.

Quick and digital setup without legal advice: An online foundation does not have its own legal form, but is established within an existing trust foundation. Therefore, setup can be done within a few minutes and completely without the support of consultants. Setting up an online foundation on bcause is much more like opening a social media account.

Low costs: The costs for an online foundation are far below those of starting a classic foundation (between 170 and 500 euros instead of several thousand euros).

Suitability: Using an online foundation is equally suitable for private individuals, families, businesses, and public figures, and for all asset sizes.

Suitable as an entry point into philanthropy: Due to the low cost, flexibility, and fast implementation, the online foundation is ideal for a first entry into philanthropy.

Advantages of the online foundation

On platforms like bcause, you can create an online foundation in just a few minutes, which offers you all the advantages of a foundation. It is also very flexible in terms of specifying and changing the foundation purpose at any time. And you save significant costs that you would otherwise spend on consultants and authorities.

Disadvantages of the online foundation

If you wish to contribute a very high amount of assets to the foundation, for which you want to apply the so-called tax privilege of § 10 Abs. 1a EStG (claiming over 10 years), this is not possible with an online foundation.

The differences between a bcause online foundation and a classic foundation are explained by lawyer Alexander Vielwerth in our blog article:

👉 bcause in a tax law check with lawyer Alexander Vielwerth

Summary of the most important points

Definition and meaning of foundations

Foundations are important organizations that pursue charitable and private purposes in the long term and virtually immutably. Depending on the needs of the founders, the term allows for other legal forms, such as GmbHs or associations, alongside the legally independent foundation under civil law. Despite high incorporation costs and stricter legal requirements, foundations offer several unique features and advantages, particularly through their independence.

Legal requirements and administration

Founding deed, articles & purpose: Central basis regulating purpose, organization, and asset deployment. Careful preparation is crucial for the foundation's success.

No binding legal form: Choice between a legally independent foundation under civil law, foundation GmbHs, or foundation funds.

Minimum assets: Starting capital of at least 50,000 to 100,000 euros is recommended to guarantee the long-term feasibility of the purpose.

Tax advantages: Charitable foundations enjoy tax exemptions, but must fulfill duties and prove their charity status annually.

Would you like a free consultation?

Digital foundations on bcause

We would be happy to support you on your way to your digital foundation with a free initial consultation.

Schedule an initial consultation now

⚠️ Disclaimer: We do not provide tax advice. We do not replace a certified tax advisor. All information is provided without guarantee.

References to further literature and resources

Books and specialist literature

"Stiftungen und ihre Verwaltung" (Foundations and their Administration) by Michael Germann

A comprehensive guide addressing the legal, tax, and organizational aspects of foundation establishment and administration. It offers practical tips and examples.

"Das Handbuch der Stiftung: Leitfaden für die Praxis" (The Foundation Handbook: A Practical Guide) by Georg von Schanz

This book is a detailed reference work for all aspects of foundation establishment and management. It covers both the establishment as well as ongoing administration and legal issues.

"Stiftung und Recht: Handbuch für die Praxis" (Foundation and Law: Practice Handbook) by Ulrich P. Müller

This handbook provides a comprehensive overview of the legal framework for foundations in Germany, Austria, and Switzerland.

"Stiftungspraxis – Alles, was Recht ist" (Foundation Practice - All that is Law) by Ulrich P. Müller

A practice-oriented guide dealing with the legal design and administration of foundations. Programmatically useful for the practical implementation of foundation projects.

"Der Stifterratgeber: Alles über Stiftungen und Nachfolgeregelungen" (The Founder Guide: All about Foundations and Succession Regulations) by Eckhart Schleifenbaum

This book gives a good overview of the different forms of foundations and their possible uses for succession arrangements and asset protection.

Websites and online resources

Stifterverband für die Deutsche Wissenschaft

The Stifterverband offers comprehensive information on establishing and managing foundations, specifically in the field of science promotion.

Association of German Foundations (Bundesverband Deutscher Stiftungen)

The Federal Association offers a wide range of information and materials on foundation establishment and administration. Here you will also find current statistics and reports on foundations in Germany.

German Foundation Centre (Deutsches Stiftungszentrum)

www.deutsches-stiftungszentrum.de

This platform offers well-founded advice on the establishment and management of foundations as well as information on legal and tax aspects.

Bertelsmann Stiftung

The Bertelsmann Stiftung offers numerous publications and studies on various social topics that may be of interest to foundation creators.

Online portal "Stiftungsexperte"

A platform specifically addressing the needs of foundation creators and administrators, providing practical tools and information.

About the author: Nicole is Chief Legal Officer at bcause and answers complex legal and infrastructural questions around foundation establishment, trust foundations and funding flows. She is also the managing director of our bcause Trust Foundation. Nicole led legal departments at PayPal and Groupon and worked as an attorney.

Sign up for our newsletter and never miss a thing.

⚠️ Disclaimer: We do not provide tax advice. We do not replace a certified tax advisor. All information is provided without guarantee.

Written by

Nicole Weyde